We have been doing a deep-dive investigation into Payvision Amsterdam’s business activities. Payvision is a 100 per cent subsidiary of one of the world’s most reputable banks, ING Groep N.V.

We know that Payvision wilfully served scammers like Gal Barak and Uwe Lenhoff, as described in our article here.

Payvision was busy doing business with other high-risk merchants in the Porn and the gaming business, too. And recently, we learned that Payvision is a defendant in several U.S. court cases initiated by high-risk U.S. merchants.

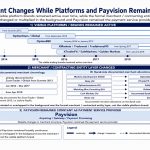

PAYVISION´s involvement in U.S. court cases

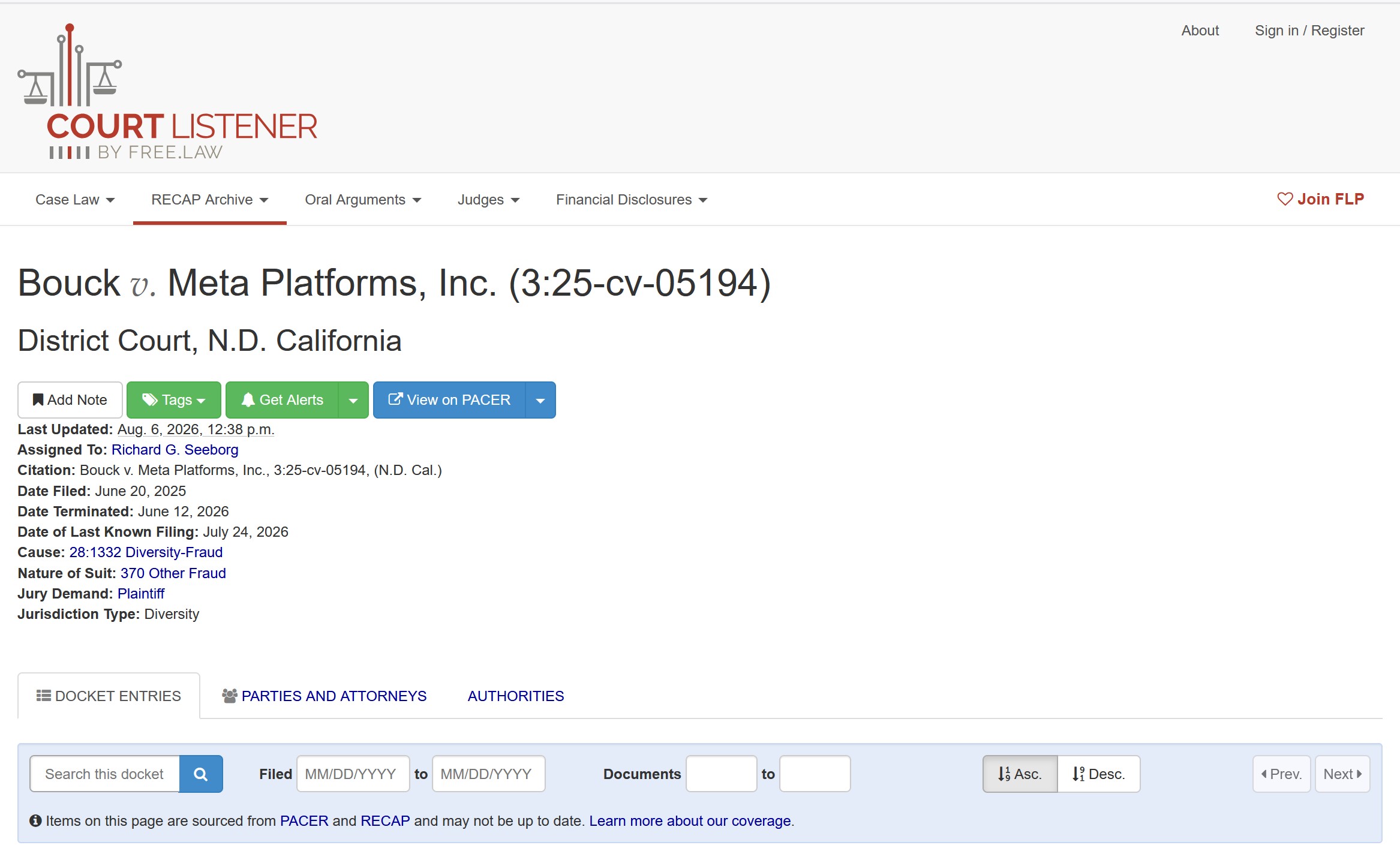

As of July 28, 2020, a legal dispute started at the United States District Court of Nevada (Case 2:20-cv-01405-JCM-VCF) between Beyond Wealth PTE LLC, UTAH (“Beyond Wealth”) – a U.S. MLM company – and T1 Payments LLC – its presumed U.S. Payment Facilitator regarding T1 Payments’ withholding a termination amount of more than 4 Mio USD. As of August 24, 2020, Payvision Amsterdam shows up in the claim as a Counterclaim-Defendant.

Beyond Wealth[3] claimed that T1 Payments LLC (“T1 Payments”), in its claimed capacity as a Payment Facilitator[4], lured them into a Merchant Service Application and Card Payment Processing Agreement in May 2020 by representing that it would provide them with bona fide and honest payment processing services.

Only weeks later, the contractual relationship went sour. Beyond Wealth found that T1 Payments was not a registered Payment Facilitator at all, and that T1 Payments’ ability to process Beyond Wealth’s transactions depended on Payvision’s violation of Card Brand (i.e., Visa and Mastercard) regulations. Beyond Wealth claims that T1 Payments is guilty of illegal access device fraud, wire fraud, bank fraud, money laundering, and unlicensed money transmission, in connection with an unlawful conspiracy with PAYVISION in Europe.

The legal claim describes in detail how Payvision processed all transactions for Beyond Wealth (a U.S. company) by creating a subaccount for Beyond Wealth under T1 Payments’ master merchant account. There was no contract between Beyond Wealth and Payvision, so T1 Payments held a merchant account under its name with Payvision. Payvision deposited the processed funds directly into the T1 Payments bank account with Atlanta Bank.

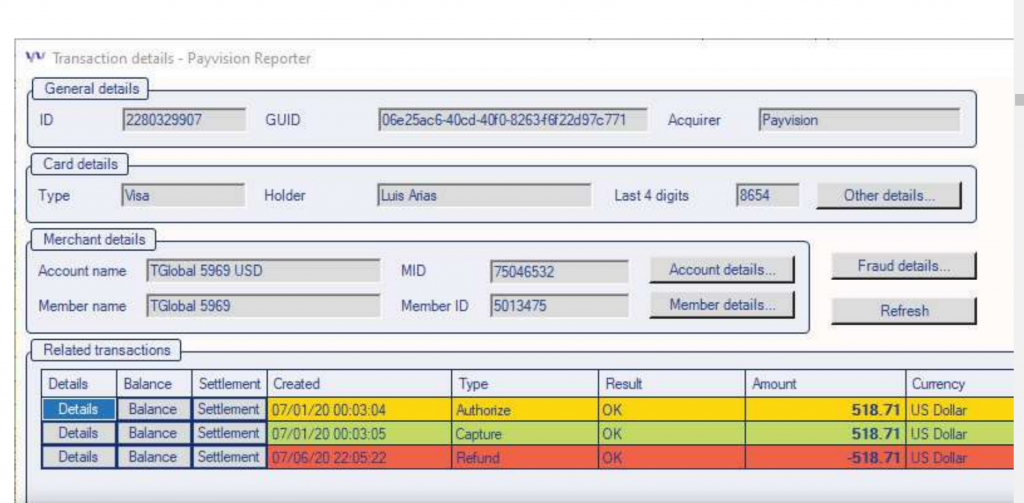

Beyond Wealth claims that T1 Payments, a U.S. company with operations exclusively in Nevada, deliberately established the U.K. shell companies T1 Payments Ltd (T1U.K.) and TGlobal Services Ltd (TGlobal). These European shell companies enabled T1 Payments to process virtually all the merchant transactions it sponsors through an undisclosed European acquirer. Payvision contracted only with T1UK or TGlobal in the UK.

Beyond Wealth LLC was also asked to create a shell company, Beyond Wealth U.K., to bring Beyond Wealth’s business to Payvision. So, although the customer payment processing agreement (CPPA) was a direct agreement between T1 Payment LLC and Beyond Wealth LLC, T1Payment submitted the transactions under the U.K entity’s name. This approach is a clear violation of Card Brand Rules.

According to the claim, T1Payments operates an incorporation formation service for its high-risk merchants. T1Payments is supposedly setting up U.K. entities for an additional fee of USD 250 as a condition for opening a merchant account with T1Payments.

T1Payments contracts with merchants under T1 Payment’s name but processes transactions through Payvision in accordance with agreements with T1UK or TGlobal.

Payvision does this even though T1UK and TGlobal are officially dormant companies, claiming to have only GBP 1 in assets.[5] The reason for this procedure is that, according to Mastercard Rule 7.1. and 7.13 any service provider’s – specifically, a Payment Facilitator’s – location must be within the acquirer’s jurisdiction. Beyond Wealth claims that by procuring U.K. shell companies for Beyond Wealth and other non-UK and non-EU merchants, T1 Payments has conspired with Payvision to create the appearance that such merchants were in the U.K. or the E.U and thus were eligible for domestic payment processing. Card Brand Rules bar T1 Payments, undisclosed E.U acquirers and payment processors from opening accounts for Beyond Wealth and those merchants.

Beyond Wealth pretends, in its claim, that the procedure for setting up U.K. shell companies is described as a standard operating procedure in T1 Payment’s onboarding instructions, the MSA, and related Materials disseminated to its partners and merchants in the ordinary course of business. The materials even discuss the possibility that merchants may need to procure an “EU Corp” in addition to their actual corporate form.

This procedure clearly qualifies as credit card laundering [6] that violates U.S. federal regulations. It represents an unlawful practice to circumvent card brand monitoring programs that prevent detection by consumers and law enforcement. Besides, it violates Dutch law, as Payvision cannot offer its licensed services to U.S. customers.

Beyond Wealth alleges that T1 Payments depends on this same structure to offer all its U.S. merchants processing services. Tens of millions of dollars have been flowing from Payvision’s bank account in Europe to T1 Payment’s bank account in the U.S., with T1 Payments forwarding the money to T1 Payment’s merchants throughout the United States.

By knowingly allowing T1 Payments to onboard merchants under an aggregated merchant account held in T1 Payments’ name, without T1 Payments being registered as a Payment Facilitator, Payvision would have conspired with T1 Payments. Beyond Wealth claims that Payvision would have participated in, promoted, facilitated, and aided and abetted that conduct while generating substantial fees.

Payvision did not verify that T1 Payments were operating a bona fide business and did not verify that T1 Payments complied with applicable law and were registered with the Card Associations. So, Payvision violated Mastercard Rules.

The PACER records show some similar cases against T1 Payments

A brief review of the PACER records indicates that there have been dozens of similar legal claims against T1 Payments in prior years. These legal claims did not prevent Payvision from doing business with this company.

Having done business with T1 Payments since 2015 and 2016[7], Payvision is familiar with these legal claims. Vantiv, a leading U.S. payment processor, filed a lawsuit against T1 Payments on March 14, 2017, in the United States District Court for the Southern District of Ohio, alleging breach of contract and fraud. Vantiv alleged that T1 Payments not only breached its agreement with Vantiv but also created fictitious entities to defraud Vantiv. It stole money from merchants by diverting funds to T1 Payments bank accounts that should have gone to the merchants. In February 2017, upon learning of the fraud, Vantiv promptly terminated its relationship with T1 Payments and caused T1 Payments to deregister with the Card Associations as a Payment Facilitator [8]. Payvision did not have these issues with T1 Payments’ practices and continued to do business with them.

An acquirer must not accept and submit transactions into Interchange from merchants, Payment Facilitators, or sponsored merchants outside the acquirer’s jurisdiction. As a Nevada-based company, T1 Payments is only eligible for sponsorship as a registered Service Provider by an acquirer based in the United States.

PAYVISION denies any wrongdoing

As of November 9, 2020, Payvision filed its reply with the court (Document 103-2), confirming that it does business only in Europe under Dutch law and complies with all Brand rules.

- The Chief Risk Officer of Payvision, Maria Alida Johana Ruijters–Terprstra, confirmed that Payvision B.V. has never sold or distributed any products or services in the State of Nevada, mainly arguing that the Nevada Court lacks jurisdiction over Payvision.

- In the court documents provided by Payvision, it gets pretty clear that Payvision has had a close relationship with T1 Payments and its U.K. shell companies for many years. Payvision attempts to substantiate its claims by citing an excerpt from its internal documents that lists the British T1 Payment companies as customers. Payvision did not explain why all the transactions shown on these internal documents in Europe are denominated in USD.

[1] Case 2:20-cv-01405-JCM-VCF United States District Court: T1 Payments LLC, Nevada, vs BEYOND WEALTH PTE LLC, UTAH and Payvision B.V., a Dutch limited company, as Counterclaim-Defendants. Fraudulent business practices dated 08/24/20

[2] Case 2: 16-cv-00739-JAD-PAL United States District Court: Atlantic Pacific Processing Systems INC vs Dermarketive (and T1 Payments LLC, Nevada)

[3] Beyond Wealth is a company that sells various products through the multilevel marketing model (“MLM”).

[4] Sometimes, Acquirers may contract with third-party organizations to provide processing related services (referred to in the Mastercard rules and hereafter as “Program Services”) to merchants under the acquirers’ sponsorship with the Cards Associations (such third party organizations ere referred to in the Visa rules as “Third-party Agents” and in the Mastercard rules and hereafter as “service providers”). A Service Provider may perform only the type of Program Service it is registered to conduct and must be registered with the Cards Association before an acquirer or merchant may use its services (see, e.g. Mastercard Rule 7.2 (The Program and Performance of Program Service).

Mastercard Rule 7.2.1 (Customer Responsibility and Control): The acquirer must at all times be entirely responsible for, and manage, direct, and control, all aspects of its Program and Program Service performed by Service Providers, and establish and enforce all program management and operating policies per Card Association Rules. An acquirer must not transfer or assign part of its responsibilities or in any way limit its responsibility to any of its Service Providers. An acquirer must conduct meaningful monitoring of its Service Providers to ensure ongoing compliance with Card Association rules.

A payment facilitator enters into contracts with acquirers to provide payment services to merchants, and it enters into a separate agreement with each merchant to enable payment acceptance. When a cardholder makes a purchase, the merchant routes the transaction data for processing through the payment facilitator’s master merchant account. A payment facilitator enters into contracts with acquirers to provide payment services to merchants, and it enters into a separate agreement with each merchant to enable payment acceptance. When a cardholder makes a purchase, the merchant routes the transaction data for processing through the payment facilitator’s master merchant account.

[5] Compare Companies House register

[6] Processing one company’s transactions through another company’s merchant account. Credit card laundering may involve opening a merchant account through a “straw” company or aggregating transactions from other companies and processing them through a single “funnel account” held in the name of the ISO, as happened here. The Department of the Treasury’s Financial Crimes Enforcement Network (“FINCEN”) regards such activities as a variation of money laundering.

[7] According to the declaration made by Maria Alida Johanna Ruljters-Terpstra (Filed 11/09/20 in Case 2.20-cv-01405

[8] Public available