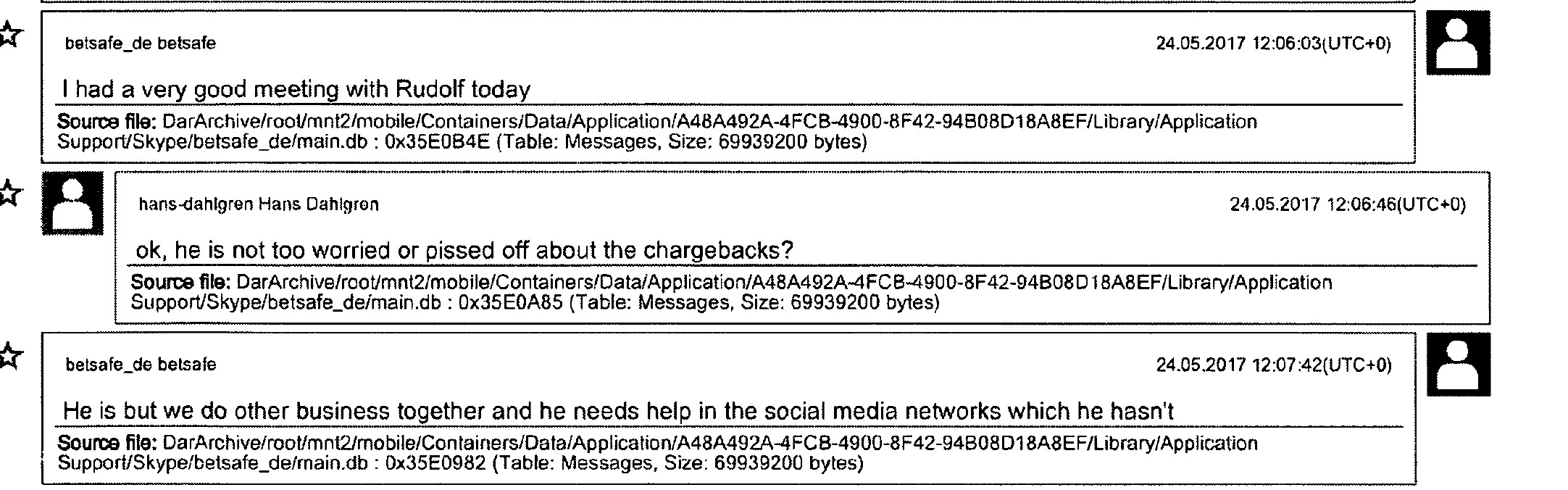

Although financial institutions worldwide step up their efforts in fighting criminals from using their systems for money laundering, more than 99% of money laundering proceeds remain in the hands of criminal gangs. It’s not just the massive amounts of money that go unseized that’s troubling (UNODC estimates that between two and five percent of global gross domestic product, which was $105 trillion in 2023), but how it emboldens these criminals involved in terrorism, drug trafficking, human exploitation, arms trafficking, fraud, tax evasion and a host of other illegal activities.

After years of researching money laundering cases in Europe, we are convinced that the primary reason AML regimes are failing is the ineffective and inefficient enforcement of money laundering laws. Prosecutors and supervisory authorities still do not seem to grasp how crucial effective anti-money laundering enforcement is in preventing online fraud, human exploitation, and drug trafficking.

Based on five examples, we will demonstrate the unwillingness of the European authorities to hold the payment industry responsible for severe money laundering:

Five revealing examples for ineffective AML enforcement in Europe!

Over the past four years, we have reviewed court documents related to cybercrime trials in Austria and Germany. Additionally, we have analysed the bank vouchers of more than 1,300 victims of transnational cybercriminal organisations. Through this research, we traced the money flows of over 1,500 victims, identifying the banks and payment institutions that appear most frequently in court documents and bank records.

Based on our research, we filed extensive complaints regarding violations of money laundering rules by three licensed payment service providers in Germany (Deutsche Bank/Postbank, Wirecard AG, and Deutsche Handelsbank AG), as well as several unlicensed payment providers (P2P GmbH, B2G GmbH). We also filed a complaint regarding the Danish Kobenhavns Andelskasse’s evident non-compliance and fraud entanglement. Lastly, we filed a complaint against the Dutch-regulated payment institution, Payvision B.V.

All our ML (criminal) complaints included extensive evidence, including copies of court documents, whistleblower information, a summary of our research, and victims’ vouchers. For all cases we included the reference numbers of the court cases and the contact details of the prosecutors in charge, as all our cases relate to cross-border cybercrime.

We sent the criminal complaints to the prosecuting office in charge (place of registration of the banks and payment institutions) and copied the relevant supervisory authorities (for licensed PSPs). We offered our support, cooperation, and information to all of these authorities. Whenever we had an update on our research, we provided the information to the relevant prosecution office.

Five years after submitting the complaint documents to the relevant European authorities and requesting an investigation into various money laundering cases, we can summarise the results of the prosecutors and the supervisory authorities in charge as nothing short of a disappointment.

It is a disgrace

Based on the inaction of the European authorities (specifically, the German, Dutch, and Danish authorities), we can only summarise that the authorities in the different countries lack an understanding of the critical role of the payment industry as gatekeepers in cybercrime incidents.

With Germany increasingly infiltrated by mafia organisations and the Netherlands being referred to as a ‘Narco State’ (see also the shooting of the journalist Pieter R. de Vries), the effectiveness of law enforcement agencies in these countries when it comes to significant money laundering cases is truly concerning.

No cross-border investigations, insignificant or absurd penalties, no use of the ‘naming and shaming’ approach, close cooperation with the white-collar lawyers of the cybercriminal enablers, disregard for the victims’ voices, and worst of all, the promotion of a prosecutor to an international position (EPPO) after they successfully abandoned a significant money laundering case just are some of the experiences we had during the past years.

Summarising, we are more than concerned about the authorities’ inexperience and unwillingness to address the cybercrime threat properly and to handle money laundering cases effectively.

Only recently, the FATF President T. Raja Kumar stated, “Global financial integrity is critical for economic stability, inclusion, and peace and security and can only be achieved through the robust and effective implementation of money laundering and terrorist financing standards.

Not holding money launderers adequately accountable results in them continuing their activities with even greater confidence and recklessness. But we also have some insights in this respect, which we will also share in the following detailed stories about Deutsche Handelsbank (nowadays: DKAM Capital GmbH) (Part I), Wirecard Bank AG(Part II), Deutsche Bank/Postbank (Part III), Kobenhavns Andelskasse (Part V), Payvision B.V. (Part VI).

Story to be continued soon: First example: Deutsche Handelsbank or as it is called now: DKAM Capital GmbH.