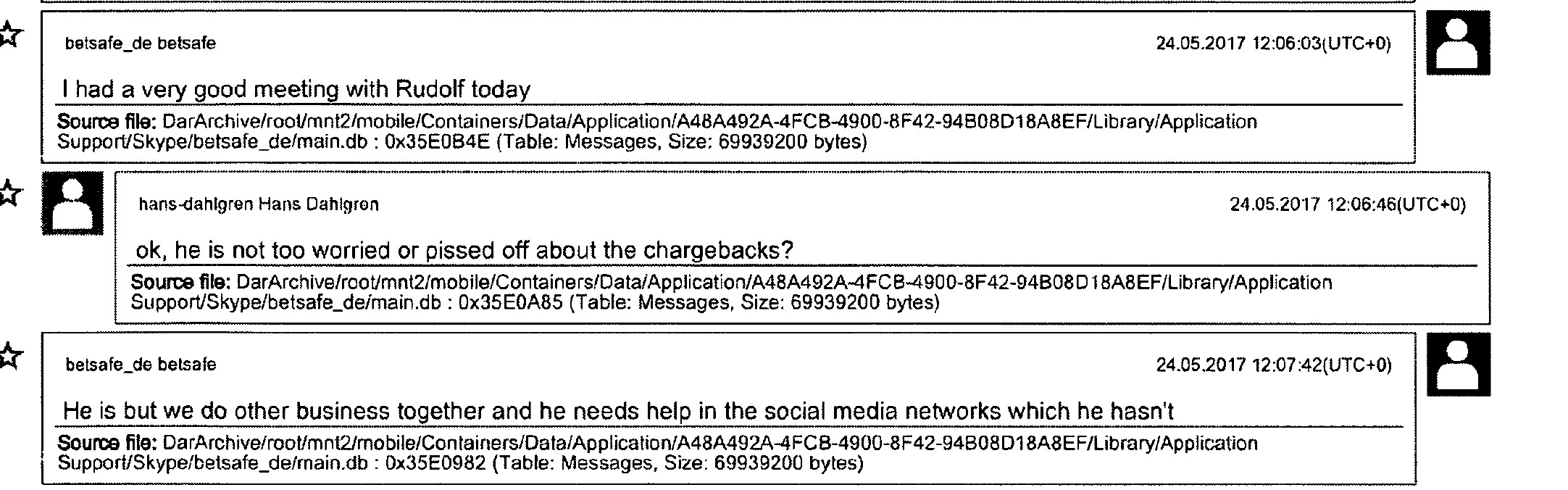

In preparing the civil legal claims against PAYVISION B.V., we dig deeply into the criminal files for Option888 and the Wolf of Sofia. We learn a lot about how these fraudulent schemes work. In addition, we also know a lot about the enablers of these enormous fraudulent activities. Unscrupulous regulated payment processors like PAYVISION B.V. and WIRECARD and banks like Deutsche Handelsbank and DEUTSCHE BANK, Kobenhavn Andelskasse have supported and enabled this kind of fraud for so many years. But we also learned that European authorities and supervisory regulators like De Nederlandsche Bank/DNB or Bundesanstalt für Finanzdienstleistungen/BAFIN must have turned a blind eye to these enormous fraudulent activities for so many years. Hundreds of thousands of consumers complaints got filed with these organizations. No adequate actions got taken, leaving the consumers all alone! So we request that the European supervisory authorities in specific European Banking Association/EBA finally starts to do a proper job in asking appropriate actions by the regional authorities.

The result of the European Court of Auditors special report 13/2021

As of June 28, 2021, the European Court of Auditors issued its unique statement 13/2021 about its investigation on the efficiency and effectiveness of the money laundering fight within the European Union. The report headlined E.U.’s efforts to fight money laundering in the banking sector are fragmented, and implementation is insufficient.

The European Court of Auditors detailed that during their audit, they found institutional fragmentation and poor coordination at the E.U. level when it came to actions to prevent ML/TF and to take action where risk was identified. In

practice, AML/CFT supervision still takes place at a national level with an insufficient E.U. oversight framework to ensure a level playing field.

Thousands of victims with millions of losses as a result of the poor performance

EFRI definitely can reconcile these findings. But the European Court of Auditors forgot to tell about the “actual” results of this poor performance on cross-border coordination and inferior performance to take actions against financial institutions involved in money laundering issues. The “actual” results are thousands of ripped off unsuspecting European consumers who lose millions of their life savings to unscrupulous criminal organizations – customers of the European financial institutions.

In Summer 2020, Wirecard, a highly celebrated German Fintech for more than ten years heavily involved in Cybercrime activities offering its payment services to the scam industry, got busted. BAFIN has received hundreds of complaints from victims but did not care.

If BAFIN had acted decisively (closing down actions) on Wirecard when the first complaints started to flow in, hundreds of people who have transferred their money via Wirecard’s account to the scammers maybe would not have been hurt.

The same is applicable for Deutsche Handelsbank. It must have been known for years already that Deutsche Handelsbank has material money-laundering issues. BAFIN did not take appropriate actions like withdrawing the banking licence but left them going on with their services for shabby e-money companies and illegal payment services companies for many years resulting in hundreds of millions of stolen money being transferred scammers via Deutsche Handelsbank.

We think that the European supervisory authorities for the payment institutions/banks/e-money institutions have to start to do a proper job and act decisively and swiftly. European supervisory authorities have to hold responsible the banks and payment processors that enable the scammers to steal the money from innocent European consumers.

The rising Cybercrime Threat

The world faces several threats, one of the newest threats we are facing, and perhaps the fastest-growing is Cybercrime. Cybercriminals, hackers and foreign adversaries are becoming more sophisticated and capable every day in their ability to use the Internet for nefarious purposes.

We are dependent on the Internet – we use it for everything. We communicate online, bank and shop online, and store much of our personal information there. The economies globally count on having ready access to the Internet and its many capabilities in our daily routines. The Internet opens new worlds to users and criminals.

The cost of Cybercrime – already in the billions of dollars and Euros – rises each year.

Why do we want EBA to get active asap?

Within Europe, Europol estimates that the value of suspicious transactions is equivalent to about 1.3 % of EU GDP. Across the globe, the figure is close to 3 % of world GDP. Recent data shows that over 75 % of suspicious transactions reported in the E.U. came from credit institutions in more than half of the Member States[1].

Financial institutions must act as gatekeepers to the financial system and have a critical role in the collective fight against the rising Cyber Threat.

The usage of the Incumbent financial system is essential to the intake of the victims’ money, to launder it and, finally, to transfer the funds to bank accounts under the direct control of the scammers.

Without their illicit proceeds used to fund criminal activities, the lifeblood of the scammers’ operations is disrupted.

Financial institutions failing to do proper customer due diligence and monitor transactions undermine citizens’ trust in financial institutions, negatively affect market integrity, and threaten the financial system’s stability.

The EBA recently got an enhanced mandate to lead, coordinate and monitor AML/CFT efforts in the European Union,

We understand that EBA should coordinate supervisory actions at the Union level to ensure that financial institutions apply effective and robust AML/CFT controls wherever they operate in the single market[2].

The EBA[3] has the power to investigate a potential breach of Union law (BUL) relating to AML/CFT legislation at the Member State level. This could involve inadequate supervision allowing large volumes of ML/TF to take place in a bank.

EBA seems to be the appropriate authority considering that cybercrime attacks like boiler room frauds do not know country borders and damage and hurt victims all over Europe.

National interests can prevent the start of a criminal investigation for money laundering, notwithstanding evident pieces of evidence.

The role of a Dutch payment institution (licensed and supervised with the DNB) in a transnational criminal organization

Already on June 5, 2019, EFRI sent numerous documents about the cooperation of PAYVISION with the criminal organizations of Gal BARAK and Uwe LENHOFF to the relevant supervisory authority in Denmark (de Nederlandsche Bank/DNB) as well as to ING for appropriate actions against the former board of management.

Up to now, we have not learned about Dutch money laundering investigations being launched at a request of DNB against the former board of management of PAYVISION resp. PAYVISION.

Despite ING supporting the idea about Environmental Social Governance (ESG) in so many press releases and stressing the importance of integrity heavily, they do not care about harmed European consumers.

Not investigating PAYVISION and the former board of management publicly for proven failure to comply with Know Your Customer rules and transaction monitoring for so many years and their evidenced involvement with criminal organizations, especially after the close personal relationship between the board of management and the beneficial owners of the criminal organizations (specifically Uwe LENHOFF) got evident, does not seem to be appropriate with all the Cybercrime Threats ahead of us and with the specific drug situation in the Netherlands.

On behalf of European victims of cybercrime attacks, we ask the E.U. authorities to finally start fighting money laundering seriously and hold the management of financial industry players responsible for supporting cybercriminal activities.

You can read the letter here.

[1] Press Release on the Report of the European Court of Auditors on The E.U. needs a more robust and more coherent oversight framework for combating money laundering

[2] https://www.eca.europa.eu/Lists/ECADocuments/SR21_13/SR_AML_EN.pdf

[3] Regulation (E.U.) No 1093/2010 of the European Parliament and of the Council of November 24, 2010, establishing a European Supervisory Authority (European Banking Authority), amending Decision No 716/2009/E.C. and repealing Commission Decision 2009/78/E.C., O.J. L 331, 15.12.2010, pp. 12-47, as lastly amended by Regulation (E.U.) 2019/2175 of the European Parliament and of the Council of December 18 2019.