Fraud does not operate on lies alone.

It operates on accounts. On payment rails. On internal transfers. On outgoing wires. On institutions willing to keep the machinery running long after the warning signs should have triggered harder questions.

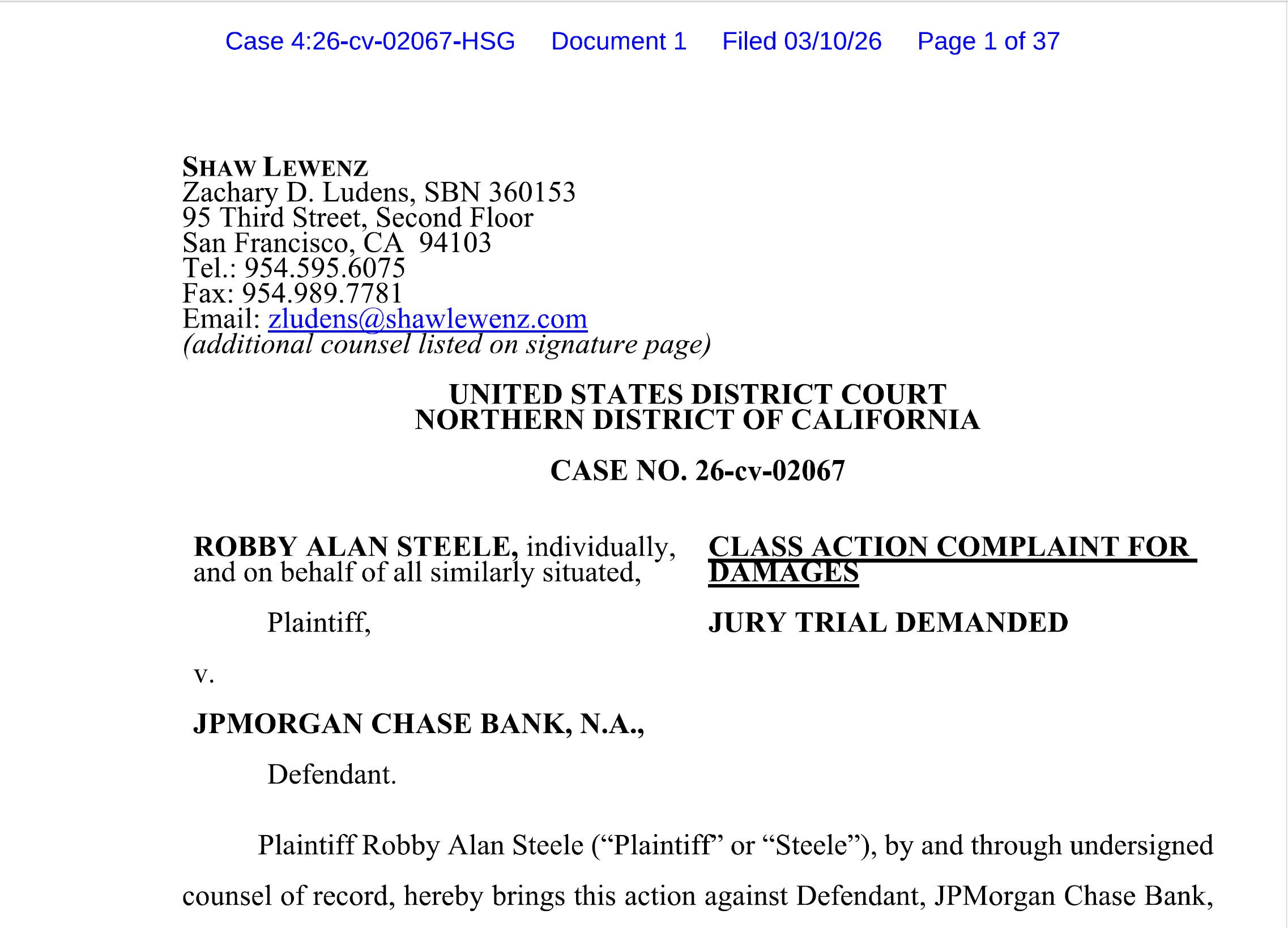

That is why the newly filed U.S. class action against JPMorgan Chase Bank, N.A. matters. Not because it is identical to the Payvision/ING case. It is not. But because the complaint captures a structure that victims in Europe have been confronting for years: a fraud system does not scale unless regulated financial infrastructure allows victim money to enter, move, and reappear as fake legitimacy.

This is not just a fraud case. It is an infrastructure case.

According to the complaint, the alleged Goliath Ventures scheme raised at least $328 million from more than 2,000 investors. The plaintiff alleges that JPMorgan provided the account infrastructure through which investor money was received and moved. The pleading further alleges that very substantial sums were transferred onward, including more than $120 million to Coinbase, and that large transfers also reached the alleged scheme operator personally. It also alleges that purported “returns” paid to investors did not come from real profits, but from money deposited by newer investors.

That last point is critical.

The complaint does not merely say that suspicious money entered and left an account. It says something much more serious: that the account activity allegedly reflected a classic fraud pattern in which new investor funds were used to pay earlier investors, while other transfers allegedly flowed to the fraudster himself. In other words, the banking system was allegedly not just adjacent to the fraud. It was part of the mechanics by which the fraud sustained itself.

The part European victims should not miss

F matter, this structure is painfully familiar.

The platforms may be different. The product story may be different. The jurisdiction is certainly different. But the operational logic is close enough to matter.

In the Payvision/ING matter, the central issue has likewise never been only the website, the call centre, or the direct fraudster. It has been the role of the regulated financial infrastructure through which victim money entered the system, was pooled, and then moved onward through merchant, settlement, and recipient structures. According to the Payvision material, victim card payments were collected through the Stichting Trusted Third Party Payvision framework, including the ING-held account NL97INGB0660731428, and funds were then routed onward through Payvision-linked structures and, in documented instances, to third-party or connected recipients.

That is why this new U.S. complaint matters. It states openly what too many courts still hesitate to confront: the financial pathway is not a side issue. It is often the operating core of the scheme.

The most important allegation in the JPMorgan complaint

One feature of the JPMorgan pleading deserves special attention.

The complaint alleges not only that investor money was collected and moved, but that large transfers were made to the alleged fraudster himself, and that purported returns to investors were funded out of later investor deposits rather than legitimate investment profits.

That is exactly the kind of pattern that destroys the fiction of neutral account activity.

Once a system is alleged to operate by:

- taking in new investor money,

- using some of it to pay earlier investors,

- and sending major transfers to the operator personally,

the legal issue is no longer whether a bank serviced an ordinary customer who later turned out to be problematic. The issue becomes whether the account activity itself allegedly displayed a pattern that should be examined as part of the fraud’s operating structure.

That is the strength of this complaint. It is not limited to generic “red flags.” It points to specific money movement logic.

Why this matters for the Payvision/ING analysis

The Payvision/ING case has always involved a more layered structure than a simple account in the fraudster’s own name.

That is one of the reasons the case is harder.

According to the existing record, the relevant flows moved through a regulated payment institution / stichting / settlement structure, not just through a plainly labeled fraud account. ING’s obvious response is that it was dealing with a licensed payment institution structure, not directly with a named fraud operator. That is a real distinction.

The real question is whether the relevant accounts were used only for ordinary safeguarded settlement, or whether the documented flows show something more: repeated outgoing transfers, third-party recipients, connected entities, and patterns inconsistent with what a neutral safeguarding structure is supposed to do.

This is where the JPMorgan complaint becomes useful by comparison. It reminds courts that the decisive issue is not the label on the account. The decisive issue is what the money was allegedly doing inside the structure.

ING’s position is even more serious for another reason

The ING dimension is not only about account provision.

By 2018, ING was not merely an outside bank. It had acquired a majority interest in Payvision and had entered into a partnership structure under which ING accounts were used in connection with Payvision’s business.

There is an additional element that should not be ignored. ING was itself operating under the shadow of a major Dutch AML investigation and settlement while acquiring Payvision and integrating it into the group structure. That does not prove liability on its own. But it materially weakens any attempt to present ING as institutionally naive about high-risk payment and AML exposure.

So the comparison with JPMorgan is not superficial. It sharpens the right question:

When a bank provides the account layer, and when that bank also becomes the group owner of the payment institution using that layer, how long can it still claim to be merely neutral infrastructure?

What the JPMorgan complaint gets right

The complaint gets one thing exactly right: it treats money movement as evidence of function.

That is the correct lens.

If victim funds come in, are pooled, are redirected, are used to pay supposed gains to earlier victims, and are also transferred in large amounts to the alleged fraudster, then the fraud is not happening “around” the financial system. It is happening through it.

European courts should stop treating this as background noise

For years, victims in the Payvision/ING matter have been told, explicitly or implicitly, that the real problem lay elsewhere: with the websites, the boiler rooms, the scripts, the false promises.

But fraud on this scale requires more than lies. It requires systems willing to receive money, process it, hold it, transfer it, and help maintain continuity.

The new JPMorgan complaint says that directly. It alleges that investor money moved through the bank, that large amounts went onward to the fraudster, and that false investor “returns” were funded from later victims

That is not a side issue. That is the operating model.

The core question is:

When the financial infrastructure receives the money, holds the money, routes the money, and helps create the appearance of a functioning investment business, can it still insist that it was merely standing nearby.