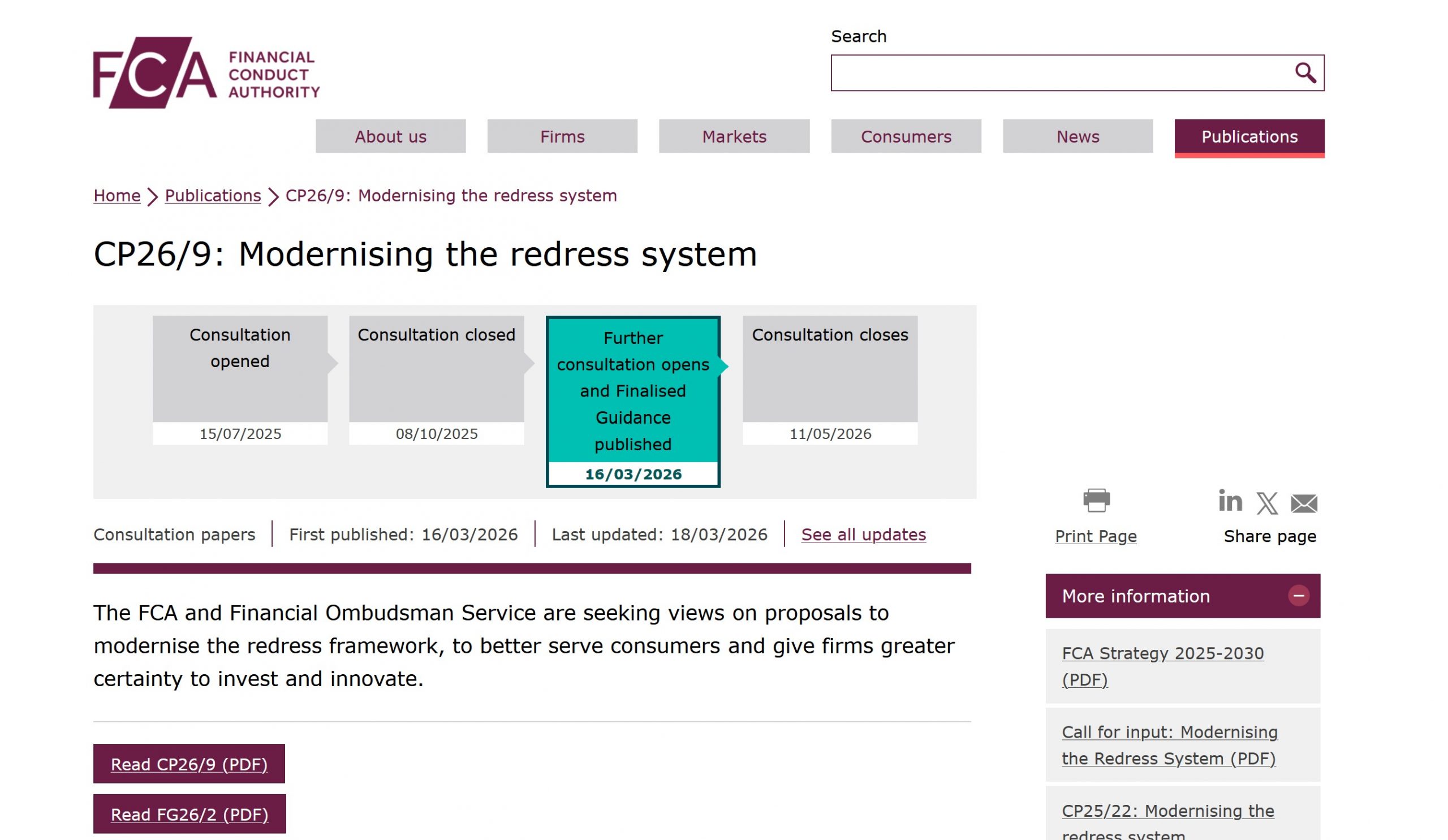

The UK Financial Conduct Authority and the Financial Ombudsman Service have launched CP26/9, “Modernising the Redress System”, presenting it as a package designed to improve predictability, transparency and early intervention in consumer redress. The FCA says the aim is to create a smoother system for consumers while giving firms greater certainty.

That is the official framing.

But the deeper question is different: when regulators promise “efficiency”, who is really being protected from friction — consumers, or the firms facing complaints?

That question matters because the package does not merely tidy up procedure. It proposes a more structured complaint gateway, broader dismissal powers, and a narrower formulation of the Ombudsman’s “fair and reasonable” test. The FCA and Ombudsman explicitly state that the package includes a new registration stage, updated dismissal grounds, and clearer guidance on the fair and reasonable test.

And that is precisely where the warning signs begin.

Which? is not persuaded

The most important external reaction so far comes from Which?, one of the UK’s best-known consumer organisations. In its published response to the earlier FCA/FOS reform consultation, Which? said it was “not convinced that the evidence presented sufficiently justifies some of the structural and legislative reforms proposed in the reform package.” It also warned that “some of the proposed structural and legal changes would detrimentally affect consumers’ access to simple, fair, impartial dispute resolution.”

That is not a technical drafting quibble. It goes to the heart of the reform.

Which? also stated that the existing redress framework already enables the aim of several proposed legislative changes, and that it does not believe major structural or legislative change is required to ensure continued access to simple, impartial and timely dispute resolution.

That critique deserves more attention than it is likely to receive.

Because once a regulator begins redesigning access to dispute resolution in the language of operational efficiency, there is always a structural risk: the complaint system may become better at managing complaint volumes than at delivering justice.

What CP26/9 would actually change

According to the FCA and the consultation paper, the current package has two main parts.

First, it contains new consultation proposals by the Financial Ombudsman. These include:

- a registration stage before full case allocation,

- changes to the grounds for dismissing complaints, and

- amendments to the fair and reasonable test in DISP 3.6.4R, including removal of the reference to “good industry practice” and clarification that only standards applicable at the time of the act or omission should apply.

Second, it already finalises parts of the earlier reform agenda, including:

- guidance in SUP 15 on when firms should report emerging issues,

- non-Handbook guidance on identifying and rectifying harm, and

- rule changes intended to improve operational efficiency at the Ombudsman and the FSCS.

The formal consultation on CP26/9 closes on 11 May 2026.

The real risk: access barriers dressed up as process reform

Some observers will say this is all sensible housekeeping. That reading is too comfortable.

A registration phase may sound harmless, even practical. Which? itself said it is supportive in principle of a registration phase, but only if it does not affect access to dispute resolution, particularly for vulnerable consumers.

That caveat is the whole issue.

In theory, a front-end registration stage screens out cases that are not ready. In practice, it can do something else: it can move burden, delay and procedural failure onto the complainant, especially where the complainant is unrepresented, vulnerable, traumatised, elderly, or dealing with complex financial misconduct.

That is the blind spot in many “modernisation” exercises. They assume that filtering improves quality. Sometimes it does. But in consumer finance disputes, filtering can also reward the better documented, better represented and better resourced side, which is rarely the consumer.

The narrowing of “fair and reasonable” should alarm consumer advocates

One of the most consequential proposals is the change to the Ombudsman’s fair and reasonable framework.

CP26/9 says the proposal is to remove reference to the Ombudsman considering “good industry practice” and to make clear that only the standards applicable at the time of the act or omission complained about will apply.

This is being presented as a clarification. It is more than that.

The Ombudsman exists in part because strictly formal legal rights are not always enough to deliver fair redress in mass consumer finance disputes. If the operative standard becomes narrower, more time-locked, and more detached from how misconduct is understood in practice, then predictability for firms may increase — but at the cost of flexibility for consumers.

That may be attractive to institutions. It is not obviously attractive to justice.

And this is where EFRI sees a broader pattern: when redress systems are recalibrated to reduce uncertainty for firms, the burden of that certainty often lands on those with the least procedural capacity to bear it.

Which? also flagged risks around lead complaint processes

Which? did not oppose every reform element. But where it did support ideas in principle, it did so with explicit conditions. On lead complaints, for example, Which? said it had concerns about the impact on access to timely dispute resolution, and warned such a process could be confusing and frustrating for affected consumers unless sufficient safeguards are built in.

Again, the same pattern appears.

A lead-case model can help manage systemic issues. But it can also suspend individual momentum, mute individual facts, and leave complainants trapped in process design choices they did not make and cannot control.

For consumer organisations, the lesson is simple: administrative coherence must never become a substitute for individual redress.

The official narrative is certainty. The institutional effect may be containment.

The FCA says the purpose of the wider reform agenda is to create greater predictability, certainty and transparency, with firms taking earlier responsibility to identify and address redress issues.

On paper, that sounds balanced.

But consumer advocates should read the package for what it may become in practice: a system that becomes better at:

- sorting,

- holding,

- sequencing,

- dismissing,

- and narrowing,

while claiming to remain fully accessible.

That is not a hypothetical concern. It is exactly why Which? says the evidential case for major reform has not been made, and why it warned that some of the proposed changes could harm access to simple, fair and impartial dispute resolution.

Why this matters beyond the UK

This is not just a British technical debate.

Across Europe, financial redress systems are under pressure from volume, complexity, institutional risk and political sensitivity. When a major regulator like the FCA moves toward a more filtered and more controlled complaint architecture, others will watch closely.

That means consumer groups should also watch closely.

Because once the logic is accepted that complaint systems must be redesigned to reduce uncertainty for firms, the next step is often predictable: more gatekeeping at the front, less discretion at the back, and more procedural reasons why consumers never reach a substantive outcome.

That is why reforms like CP26/9 must be judged not by how neat they look on a flowchart, but by a harder metric:

Will more harmed consumers obtain fair outcomes — or will more of them be held at the threshold?