Crypto coverage is already treating the Uniswap dismissal as another big win for the sector. That reaction is understandable, but it overreads the judgment. On 2 March 2026, Judge Katherine Polk Failla dismissed the Second Amended Complaint with prejudice in the class action Risley v. Universal Navigation Inc. Yet the ruling is best understood as a pleading-failure decision, not as a sweeping declaration that DeFi platforms are beyond the scope of fraud law. Properly read, the Uniswap case shows what a poorly built lawsuit looks like, not what a risk‑free future for DeFi platforms will be.

What the Uniswap Case Actually Decided

In the Uniswap case, a U.S. federal court dismissed a class action brought by investors who had purchased so‑called scam tokens through the Uniswap protocol. The plaintiffs tried to hold Uniswap Labs and its founder liable on the theory that the protocol enabled rug pulls and fraudulent token offerings. Specifically the complaint addressed the following claims:

Federal Securities Claims (Dismissed Early)

The original and first amended complaints (filed in 2022) included extensive federal securities law violations, which were dismissed by Judge Failla in August 2023 and upheld by the Second Circuit in February 2025.

Section 5 of the Securities Act: Alleged Uniswap operated as an unregistered securities exchange by allowing scam tokens to be traded without registration.

Section 12(a)(1): Claimed Uniswap sold unregistered securities through its smart contracts and protocol.

Section 15: Control person liability against Hayden Adams and venture capital backers (e.g., Paradigm, Andreessen Horowitz) for the above violations.

Section 29(b) of the Exchange Act: Uniswap’s smart contracts were deemed collateral to third-party scams, not sufficient for voiding contracts or liability.

These claims failed because the court found no convincing basis to treat Uniswap as a traditional exchange or broker-dealer; the protocol was seen as neutral infrastructure

State Law Claims in Second Amended Complaint (SAC, May 2025)

After the appellate remand, the SAC dropped federal securities claims and focused on six state-law theories against Uniswap Labs and Adams only. The March 2026 opinion dealt with the re-pleaded state-law theories, not the whole universe of possible liability questions in decentralised finance. Notably, the opinion also recognizes that one way investors accessed the protocol was through a web interface controlled and hosted by Labs, which makes the case more specific than the slogan “code alone cannot be liable” suggests. All were dismissed with prejudice on March 2, 2026.

Claim | Jurisdiction/Basis | Key Allegation | Why Dismissed |

Aiding and abetting fraud | Common law (NY) | Uniswap knew of specific scams (e.g., MXS, BUNNY, AWF tokens) and substantially assisted by providing the marketplace and fees. | No plausible facts showing actual knowledge of fraud or substantial assistance beyond neutral platform access. |

Aiding and abetting negligent misrepresentation | Common law | Uniswap facilitated misleading token promotions via its protocol. | Failed to allege knowledge of deceptive conduct or active role in misrepresentations. |

Consumer protection violations | NY General Business Law §349, NC Unfair Trade Practices Act, ID Consumer Protection Act | Deceptive practices by enabling scam token trades, harming consumers. | No proof of deceptive acts by Uniswap itself; mere facilitation insufficient. |

Unjust enrichment | Common law | Uniswap profited from trading fees on scam tokens without providing value. | Plaintiffs couldn’t show Uniswap’s enrichment was at their direct expense or unjust. |

The court requested "subjective knowledge"

The core of the judgment lies in the court’s treatment of knowledge. Under the New York aiding-and-abetting framework used here, the plaintiffs had to plead that Uniswap Labs had actual knowledge of the underlying fraud. Judge Failla expressly rejected constructive knowledge, recklessness, willful blindness, and even what she called a “forest of red flags” as enough. She also held that emails sent after purchases, public user complaints, and a study about scam prevalence on the protocol did not create a strong inference that Uniswap Labs knew about the specific frauds affecting these plaintiffs at the relevant time. That is the central reason the decision should not be exaggerated. The court did not say that platform knowledge can never be shown. It said this complaint did not show it with the specificity the law required.

The evolution from 14 federal claims (original complaint) to 6 state claims (SAC) shows plaintiffs’ adaptation, but each iteration failed on factual pleading standards: courts required concrete evidence of knowledge and assistance, not just ecosystem-level enablement

Missing substantial assistance and missing legal duty

From a consumer-protection perspective, that is the key point. The complaint appears materially underdeveloped on subjective knowledge. But that is not the whole story. The court also held that the plaintiffs had not pleaded substantial assistance. In other words, launching and operating the interface, making a marketplace available, or allowing swaps to occur was not enough by itself. The opinion stresses that the SAC did not adequately allege that Uniswap Labs promoted the scam tokens, participated in the issuers’ misrepresentations, or had a legal duty to intervene in the way the plaintiffs claimed. That means a stronger case would likely have needed not just better knowledge allegations, but much tighter facts linking Uniswap Labs’ own conduct to the frauds themselves.

Consumer Protection Claims Followed the Same Pattern

The same pattern appears in the consumer-protection counts. Judge Failla found no adequately pleaded affirmative misstatements by the defendants, rejected the omission theory because much of the relevant risk information was already public or expressly acknowledged in public warnings and the Terms of Service, and held that the complaint tied the plaintiffs’ losses to the issuers’ fraud, not to deceptive acts by Uniswap Labs. She then added that creating access to a marketplace where millions of users can lawfully swap tokens is not, by itself, unfair or unconscionable merely because fraud may also occur there. That is a pro-infrastructure instinct in the judgment, but it still rests on the pleaded facts and the specific causes of action before the court.

The unjust-enrichment claim failed

The unjust-enrichment claim failed for equally concrete reasons. The court said the complaint did not plausibly allege a specific and direct benefit to Uniswap Labs during the relevant class period. The protocol-fee theory was weak because the complaint did not allege that Labs had actually received those fees, and the interface fee was introduced only in October 2023, after the class period. Again, this shows why the judgment should not be turned into a philosophical declaration that DeFi is immune. The ruling is narrower: the pleaded economic link was too thin.

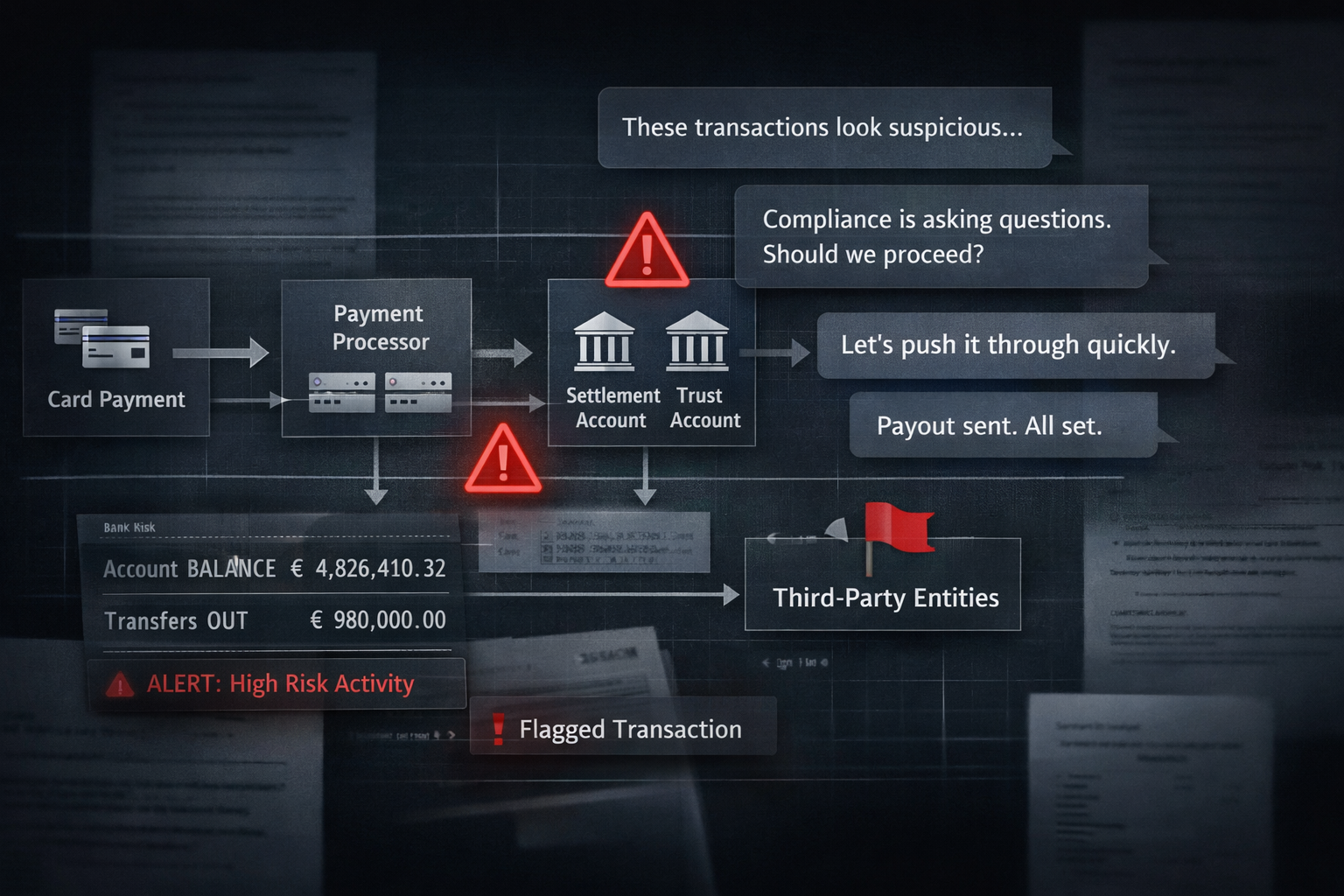

EFRI has reviewed hundreds of victim cases across payment systems and crypto platforms. The Uniswap complaint lost because it attacked an ecosystem rather than documenting actual knowledge and substantial assistance in specific frauds.