Stablecoins, on-chain crypto-assets pegged to the value of fiat currencies such as the US dollar and Euro (USDT and USDC), are currently used predominantly as the “cash leg” of the crypto ecosystem: they serve as a settlement and liquidity instrument for trading and as a bridge between fiat and crypto markets, rather than as a widely adopted method for everyday online commerce.

At the same time, their technical properties—global reach, 24/7 transferability, and low marginal transfer costs—make them increasingly attractive in cyber-enabled fraud, because proceeds can be routed rapidly across jurisdictions and converted through on-/off-ramps. Compared to Bitcoin or Ether, stablecoins minimise price risk between receipt and cash-out while preserving near-irreversibility at the transfer layer (there is typically no native “chargeback” mechanism once funds are sent). This shifts consumer protection and recovery away from traditional dispute tools toward rapid action at key gateways such as on-ramps/off-ramps, centralized exchanges, and—where available—issuer controls.

The Upcoming Chainanalysis Crypto Crime report for 2025

In its 8 January 2026 introduction to the 2026 Crypto Crime Report, Chainalysis states that illicit cryptocurrency addresses received at least USD 154 billion in 2025, a 162% year-over-year increase. Chainalysis attributes much of that rise to a 694% increase in value received by sanctioned entities, while also noting that activity increased across most illicit categories. Importantly, Chainalysis stresses this is a “lower-bound estimate” based on addresses identified to date, and that the illicit share of all attributed crypto transaction volume remains below 1%.

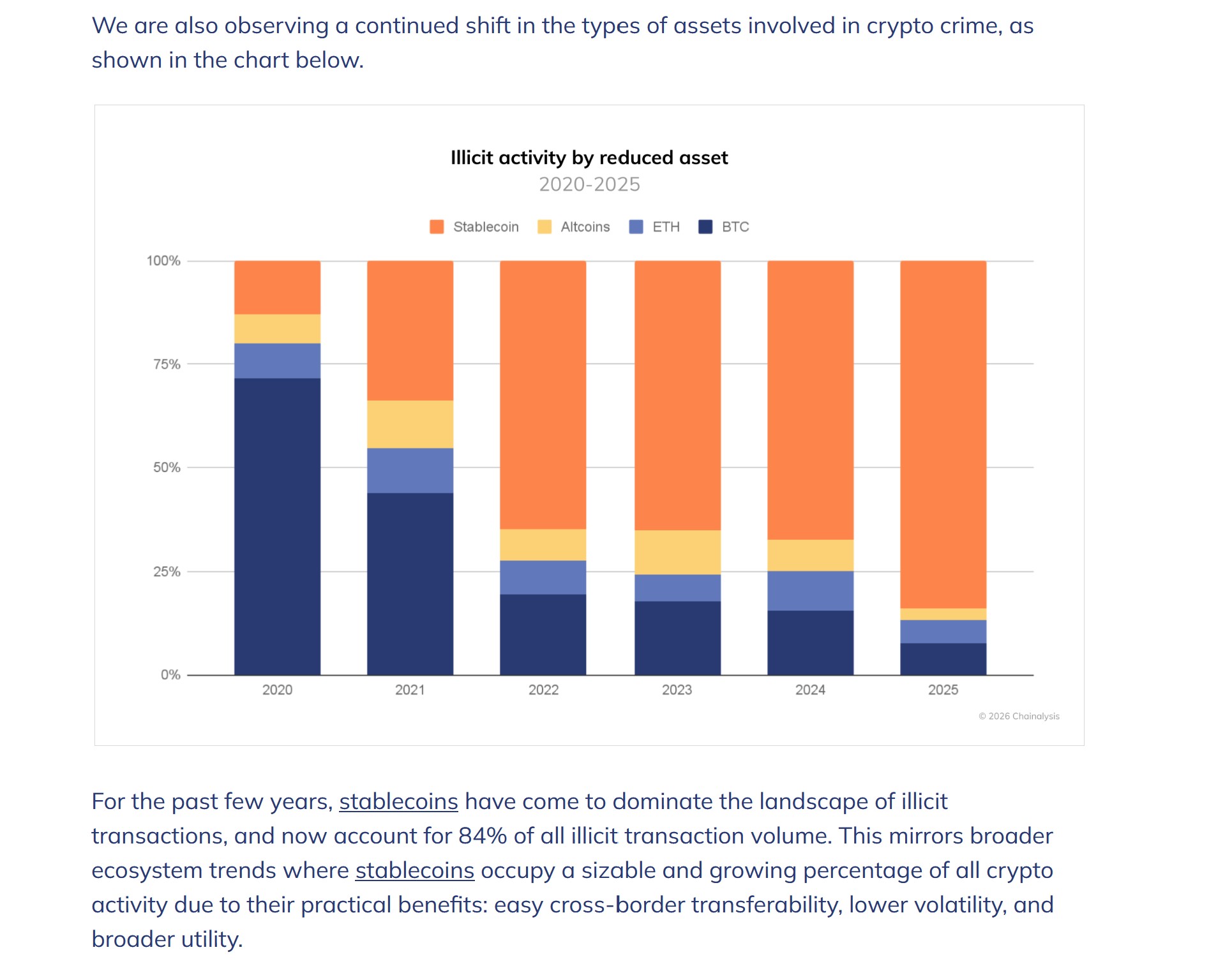

Chainalysis states: For the past few years, stablecoins have come to dominate the landscape of illicit transactions, and now account for 84% of all illicit transaction volume. This mirrors broader ecosystem trends in which stablecoins account for a sizable and growing sharecrypto activity.

On 13 January 2026, Chainalysis published a chapter focused on scams, reporting that crypto scams received at least USD 14 billion on-chain in 2025. Based on historical attribution patterns, Chainalysis projects that the 2025 figure could exceed USD 17 billion as additional illicit wallet addresses are identified. Chainalysis also highlights a surge in impersonation scams (+1400% YoY) and the increasing role of AI-enabled scam tooling and industrialised scam infrastructure.

Putting “84% illicit stablecoins” in context: how big is stablecoin usage right now?

To understand what “stablecoins dominate illicit on-chain flows” means in practice, it helps to place the illicit figures against today’s overall stablecoin footprint:

Global circulating stablecoin supply: Visa’s on-chain analytics materials cite over USD 272 billion in circulating stablecoin supply.

Stablecoin transfer activity (volume): Visa reports USD 10.2 trillion in “adjusted global transaction volume” over the last 12 months, and also cites over USD 47 trillion in overall stablecoin transaction volume over the last 12 months (depending on methodology).

Reuters reports that Tether alone has USD 187 billion worth of tokens in circulation.

So it is just a small portion yet..

Chainalysis reports USD 154B to illicit addresses in 2025, and says 84% of illicit volume is stablecoins. That implies roughly USD ~129B in illicit stablecoin flows (154 × 0.84 = 129.36).

Compared to trillions in annual stablecoin transfer volume, that is a relatively small fraction. But two caveats matter:

Chainalysis is measuring value received by (known) illicit addresses, not total network transfer volume.

“Transaction volume” metrics vary materially by methodology (gross vs adjusted; whether internal churn is filtered; which chains are covered).

So, the headline is not “most stablecoin use is illicit.” The more precise takeaway is: where crypto crime is visible on-chain, stablecoins have become the dominant instrument.

Stablecoins are the perfect payment rails for scammers

From a consumer-protection perspective, the shift toward stablecoins is operationally significant because stablecoins offer a perfect payment rail for scammers:

- Speed and 24/7 transferability (reducing intervention time),

- International cross-border reach (jurisdictional complexity) (Instant Payment rails are still regional!)

- Irreversibility of the payment transactions

- Massively lower expenses (no chargeback fees!), (no layering fees for Professional Money Launderers providing bank accounts to launder the money).

- No layering is required anymore (when scammers used wire transfers, they had to use several layers with bank accounts across Europe before sending the money to offshore bank accounts to increase opacity).

- The volatility and liquidity constraints that limited the viability of BTC, ETH and many altcoins as scam payment rails are solved mainly in the case of major stablecoins.

- High opacity from the perspective of an individual consumer

- No more payment accounts with traditional banks are necessary for merchants to receive the money.

- high liquidity and standardisation (USDT/USDC function like “programmable dollars”).

Traditional card schemes offer structured dispute/chargeback or recall mechanisms at the scheme level, making ex post reversals an integral part of the system design.

Public‑chain stablecoin transfers are technically final at the ledger level; there is no native “system operator” who can unwind a transaction, so reversals depend on off‑chain actors such as custodial exchanges, wallet providers, or courts.

Gatekeepers and Issuer controls will become more important

Summarising the substantial advantages that stablecoins confer on the scam economy, compliance duties and strict liability rules at key choke points will become critical. Centralised exchanges, custodial wallets, and other intermediaries can function as effective gatekeepers: they can freeze accounts, block withdrawals, and comply with court orders; thus, the prospects of recovery often depend on whether the funds still reside with or transit through such entities.

Certain bank‑style or permissioned stablecoin arrangements embed issuer‑level freeze and clawback controls (for example, on some Stellar‑based dollar stablecoins), enabling the issuer to block or reassign tokens in narrowly defined circumstances and thereby simulate a limited form of reversal. At the same time, experiments with smart‑contract‑based refund or chargeback layers (such as “refund protocols” or non‑custodial dispute‑resolution overlays) demonstrate that an additional, programmable dispute layer is technically feasible, but remains far from a market‑wide standard.

Against this backdrop, the notion of “stablecoin issuer controls (where available and legally triggered)” is accurate, but captures only an exceptional mitigation tool rather than a generally applicable consumer‑protection safeguard comparable to card‑based chargeback regimes.

We need a Shared Liability Framework

Considering the significant advantages that stablecoins offer to scammers, and the fact that banks and payment service providers with a record of lax AML practices are now actively entering the stablecoin market, the case for robust, strict liability rules at on‑ and off‑ramp choke points becomes compelling. In this constellation, stablecoins amplify existing structural weaknesses in financial crime controls rather than mitigating them. Taken together with the massive impact of AI on the scale, targeting and sophistication of online fraud, imposing strong, strict liability rules for these intermediaries emerges as the only realistic policy lever for addressing the escalating threat posed by the online scam industry. Please read our paper on this topic.