The big announcement

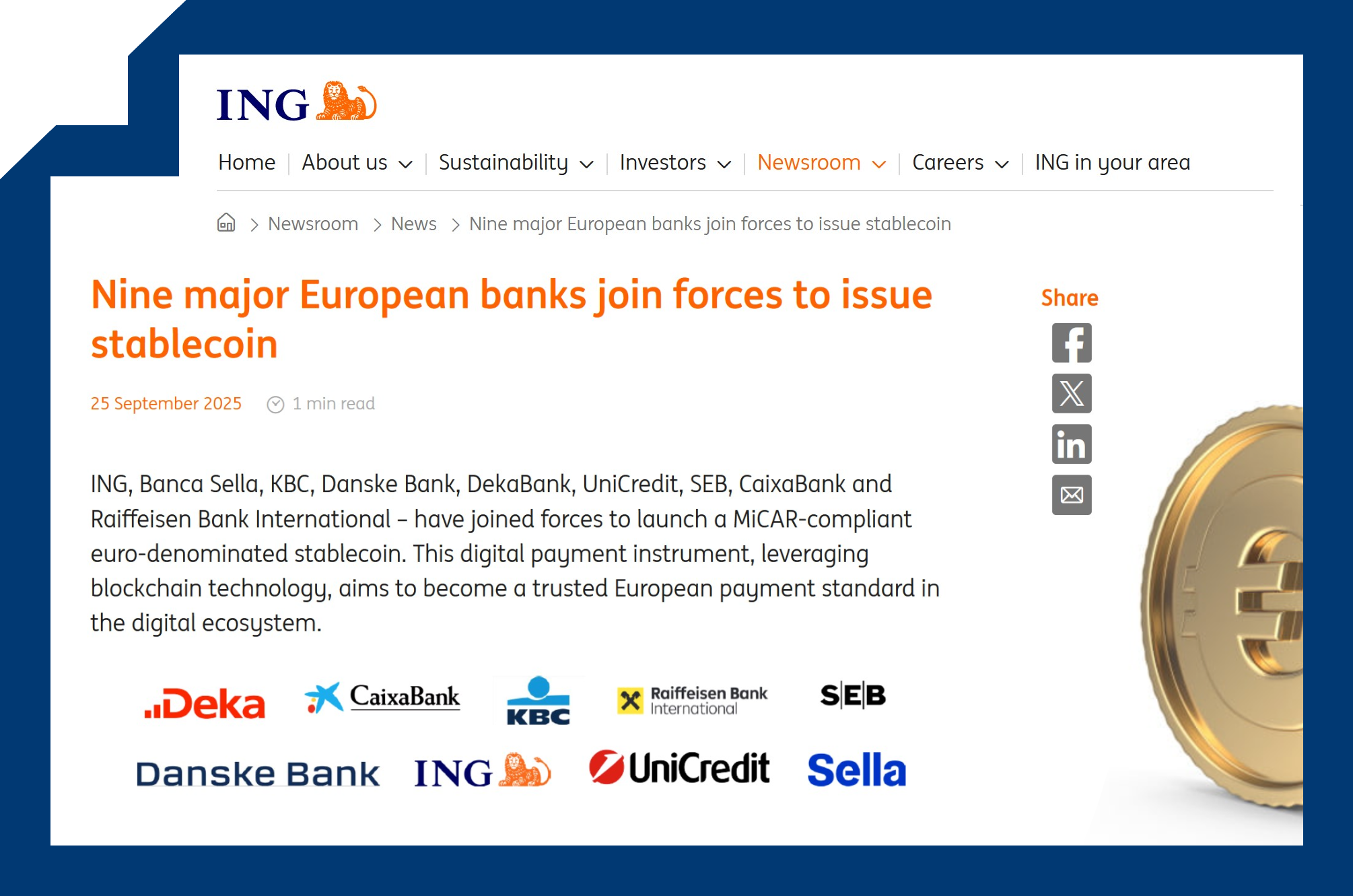

Last week, nine European banks—including ING, UniCredit, Danske Bank, SEB, KBC, CaixaBank, Raiffeisen Bank International, DekaBank, and Banca Sella—announced their intention to issue a euro-denominated stablecoin by 2026 jointly. Billed as a pan-European public–private initiative, this move is positioned as a strategic response to the increasing dominance of US dollar-based stablecoins and as a step toward Europe’s financial sovereignty in a rapidly digitising payments landscape.

Initial Reactions: Promise and Scepticism

While some industry voices welcomed the project as overdue and necessary to counter the US’s lead in digital currencies, a chorus of critical commentary has quickly emerged:

Many analysts argue that banks are arriving late, with Euro stablecoins facing entrenched competition from USD alternatives, both in terms of liquidity and integration within the global digital finance landscape.

There are doubts about whether such a product, being bank-led and heavily regulated, can capture a significant market share or will instead be relegated to niche, intra-bank use.

Regulatory hurdles remain high, with fragmented interpretation of MiCA and potential compliance issuesn for users, particularly SMEs and fintechs seeking access to programmable payments.

Systemic and Financial Stability Risks

Key policy commentators, including ECB President Christine Lagarde, have warned that stablecoins—even those issued by incumbent banks—can reintroduce “liquidity and redemption risks through the back door.” Without consistent, international standards, stablecoins risk undermining the EU’s monetary autonomy, potentially substituting central bank money with private alternatives and weakening established regulatory protections.

Moreover, the European financial system could become even more dependent on non-EU liquidity sources if adoption falters, raising concerns about long-term eurozone stability and consumer protection.

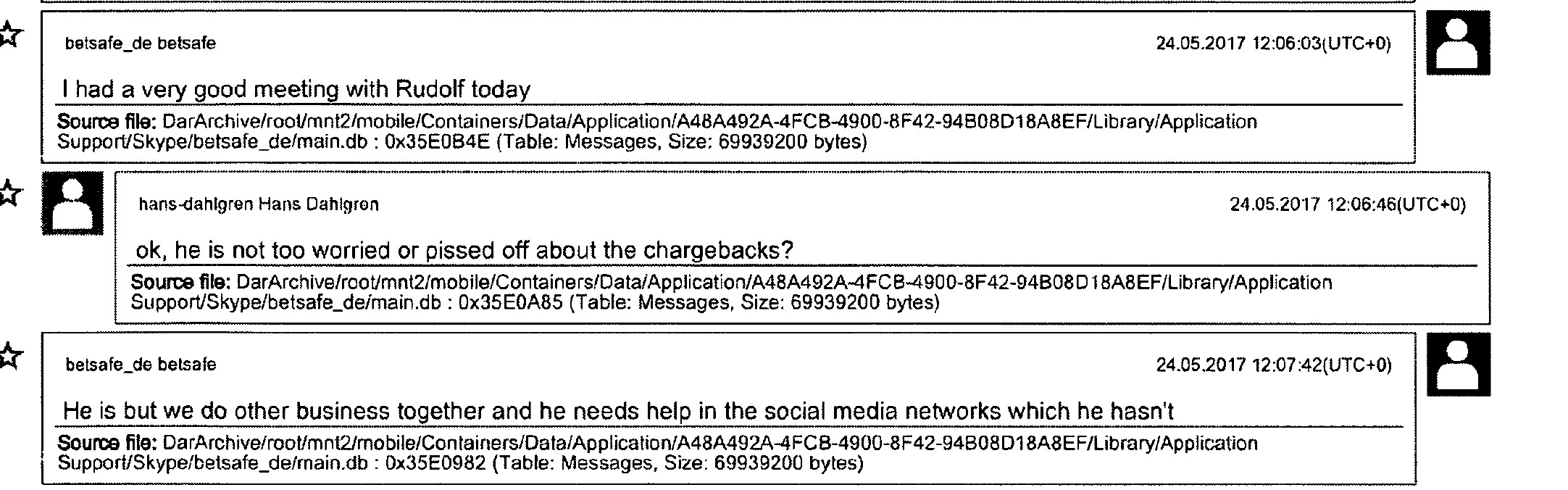

The Elephant in the Room: The Banks’ AML Track Records

Perhaps most troubling, yet largely absent from the bank-driven narrative, is the well-documented history of AML and compliance failures at the very institutions now promising to secure the future of European digital money.

ING has faced near-continuous regulatory scrutiny over the past decade, including a €775 million fine in 2018 for persistent, structural AML system failures and a culture where commercial interests allegedly trumped compliance. The bank remains under legal pressure from legacy misconduct, with continuing litigation and investor actions relating to past money laundering lapses.

UniCredit has similarly been sanctioned for billions for international sanctions violations and insufficient AML controls, including a landmark $1.3 billion US penalty for bypassing Iran-related controls and operating with “unsafe and unsound practices,” as defined by the US Federal Reserve. Requirements for third-party monitoring and remediation efforts followed.

Danske Bank‘s Estonian branch remains notorious for Europe’s largest money laundering scandal, helping non-EU clients move more than €200 billion in suspicious transactions worldwide, resulting in billion-dollar penalties and public revelations of systematic AML neglect across management and control lines.

Raiffeisen on the other hand is under significant sanction risks due to its past and still ongoing linkages to the Russian market.

The histories of SEB, KBC, and other consortium members reveal similar patterns: a focus on business growth at the expense of robust, proactive financial crime prevention frameworks.

What Does This Mean for a Pan-European Stablecoin?

It is concerning that the primary drivers behind a foundational new payments instrument in Europe are the very institutions whose AML failures helped fuel regulatory and reputational crises across the continent. A stablecoin, by definition, must guarantee transparency, redemption at par, and total integrity across its technical, governance, and compliance layers.

Given these banks’ mixed records, EFRI sees a credible risk that trust and robust risk management may be sacrificed for short-term competitiveness or market share. Without strong, genuinely independent oversight and a full commitment to compliance reform—not just at headline announcements, but in daily operational realities—the stablecoin project risks merely digitising yesterday’s governance blind spots with tomorrow’s payments technology.

EFRI's conclusion

EFRI welcomes innovation that truly enhances transparency, resilience, and consumer trust in the European payments system. However, history teaches that “technology is no substitute for robust governance and compliance culture.” We urge European authorities (especially De Nederlandsche Bank), users, and civil society to require demonstrated, sustained improvements in AML and financial crime controls from every consortium member before allowing such a systemic role in the euro payments ecosystem.

As always, we will continue to monitor the progress of this initiative closely and encourage open, critical debate about who should be trusted to anchor the digital future of European money.