We have reviewed excerpts from the criminal case files concerning B2G GmbH. These records show that although BaFin had been aware of the laundering activities of Oleg Shvartsman and Rainer Treuer since November 2017, no SARs were filed with the FIU and/or law enforcement, and payment rails remained open until the end of July 2018.

Specifically, BaFin acted swiftly in early November 2017 under the ZAG (unlicensed money transfer business). Yet the primary consumer payment rail at Sparkasse Koblenz remained operational until July 2018, even as complaints and refund demands escalated.

EFRI’s research raises critical enforcement questions about BaFin’s role as an AML supervisor and its consumer protection mandate.

Please note: EFRI does not conflate the statutory roles of BaFin, FIU, prosecutors, or banks. The question raised here concerns supervisory timing and the use of available instruments once parallel AML and criminal processes were already underway.

Background information:

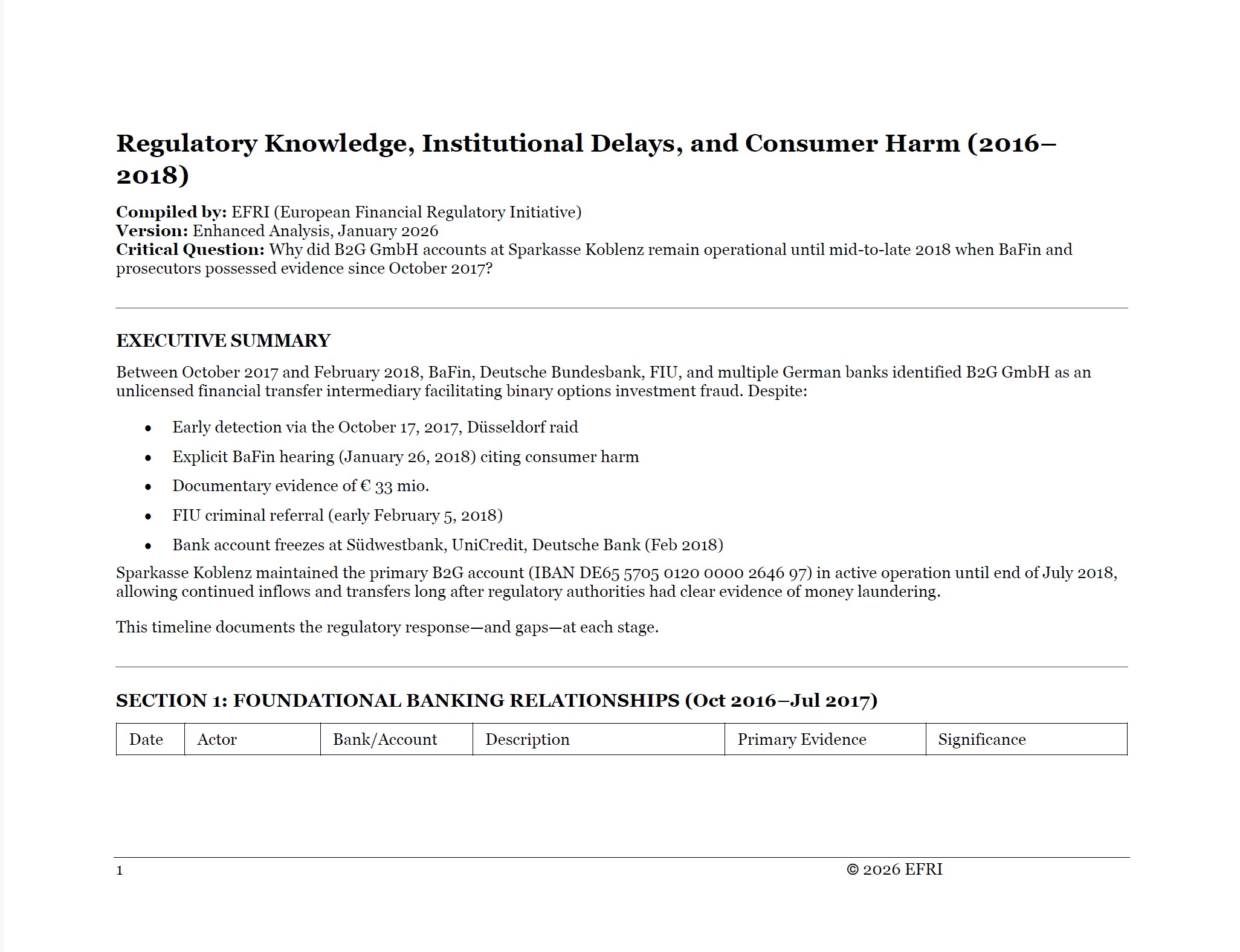

In October 2025, EFRI obtained access to the criminal case file in the ongoing proceedings against German citizen Rainer Treuer and Russian‑Israeli national Oleg Shvartsman, the beneficial owners of B2G GmbH. B2G GmbH was one of the key money mules used to launder victim deposits from a series of large‑scale investment scams (OptionStarsGlobal, Weiss Finance, InstaFx24, Blue Trading, SafeMarkets, Aspects Financial, MarketsTrading, CentroBanc, StoxMarket) between 2017 and 2018, resulting in massive losses for European citizens. B2G GmbH opened bank accounts with Volksbank Köln-Bonn, Sparkasse Koblenz, and Deutsche Bank.

The B2G case file shows that Treuer and Shvartsman also controlled P2P GmbH, another money mule that operated German and Dutch bank accounts for laundering activities during 2017–2018. Furthermore, information sent by the Hungarian FIU to its German counterpart in April 2018 revealed that Shvartsman was the beneficial owner of Fincompany s.r.o., a Hungarian money mule used in the BARAK and Lenhoff schemes, and that Hungarian records listed him as the beneficial owner of 89 additional companies with accounts at Hungarian banks. Approximately €50 million in victims’ funds were laundered through German bank accounts linked to P2P GmbH and B2G GmbH.

1) What BaFin had in hand—early and directly

17 Oct 2017: the starting point becomes “payment-rail intelligence”

The court file references the 17.10.2017 Düsseldorf search (binary options context) as the origin of evidence showing B2G accounts in deposit instructions.

14 Nov 2017: BaFin targets the banks—by name and account relationship

Based on findings in the search BaFin sends a formal §44 KWG information request to Sparkasse Koblenz and Volksbank Köln-Bonn (Kölner Bank), requesting account opening records and account overviews tied to the suspected B2G scheme context. Volksbank Köln-Bonn informed the BaFin about its termination of the banking relationship with B2G GmbH – due to numerous fraud complaints by payers, and onwards transfers including cross-border outflows to high-risk countries.

08 Dec 2017 → 17 Jan 2018: BaFin triggers a cross-bank evidence build-up via Bundesbank

The file trail documents that, as agreed with BaFin, Deutsche Bundesbank contacted the other account-holding institutes (letter dated 08.12.2017) and then delivered an evaluation to BaFin dated 17.01.2018, describing high-volume retail deposits (“Investment”/“Private Investment(s)”) and onward transfers including cross-border outflows.

26 Jan 2018: BaFin escalates on ZAG—formal hearing

BaFin issues a formal hearing to B2G on 26.01.2018, stating suspected unlicensed money transfer business activities (Finanztransfergeschäft – ZAG) and describing the payment-intermediary model in the binary-options setting.

2) Cologne prosecutor opens criminal investigation mid of February 2018

After receiving information from FIU regarding several SAR filings from Volksbank Köln-Bonn, Südwestbank, Deutsche Bank, and UniCredit, and a request to open a criminal investigation, the Cologne prosecutor (StA Köln) opened a criminal case against Treuer and Shvartsman for money laundering and unauthorised payment processing.

05.02.2018: FIU transmits operative analysis to StA Köln and recommends criminal proceedings.

16.02.2018: Criminal investigation opened (115 Js 75/18) per the matrix timeline.

By the end of February 2018, the Cologne prosecutor and BaFin (the department responsible for unauthorised payment processing) were in contact and learned that the Munich prosecutor had opened a case against Treuer and Shvartsman already in early 2017 and had conducted a search at B2G GmbH’s offices on 22 February 2018 and that the UniCredit bank account had been seized.

3) BaFin proves it can act quickly: the Südwestbank disposition ban

22 Feb 2018: BaFin orders a bank-directed restriction under §7 ZAG

BaFin issues a Verfügungsverbot (disposition ban) to Südwestbank on 22.02.2018 for the B2G relationship—account no. 324217005 / IBAN DE24 6009 0700 0324 2170 05 (as recorded in the EFRI matrix) only after the Südwestbank informs the Cologne prosecutor that they intend to terminate the banking relationship with B2G GmbH.

4) Banks closed down the payment rails by the end of 02/2018, except for Sparkasse Koblenz

EFRI’s matrix reflects that multiple banks acted earlier than Sparkasse, including SARs and terminations in 2017–Feb 2018:

Kölner Bank eG / Volksbank Köln Bonn eG

Account no. 5585868002 / IBAN DE50 3716 0087 5585 8680 02 opened 25.10.2016.

SAR filed 15.08.2017; extraordinary termination letter 22.08.2017 (effective closure deadline 30.10.2017).

Deutsche Bank (Bonn)

IBAN DE67 3807 0059 0073 7437 00 opened 18.07.2017 (plus FX sub-accounts referenced in the matrix).

SAR trail appears from Oct 2017 onward; closure is stated as 07.02.2018 in EFRI’s narrative/matrix.

UniCredit / HVB

MultipleSARs listed: 16.10 / 27.11 / 13.12.2017; 09.01 / 23.01 / 19.02 / 20.02.2018 (accounts/IBANs listed in the matrix).

At the end of February 2018 all banks except Sparkasse Koblenz had terminated their banking relationships, numerous SARs been filed, money was seized, a criminal proceedings were opened, a raid was done – but the payment rails accounts at Sparkasse Koblenz still accepted victims’ money and sent it offshore and neither BaFin nor the Cologne prosecutor told them to close down the bank accounts (three accounts were run by Sparkasse Koblenz for B2G GmbH).

5) Treuer's and Shvartsman's law firms start discussions with the BaFin for months

On 13 March 2018, B2G GmbH’s lawyer informed BaFin that B2G stopped their cooperation with the binary option clients. BaFin requested evidence.

6) The Sparkasse Koblenz “outlier” rail—complaints, refunds, and late escalation

The prosecutor/FIU material describes Sparkasse Koblenz’s B2G account as conspicuous due to numerous complaints and refund demands.

Key dates:

14.07.2017: Sparkasse Koblenz confirms the B2G business account has existed since this date: account no. 264697 / IBAN DE65 5705 0120 0000 2646 97.

12.06.2018: Sparkasse files its first documented SAR (as summarised in the evidence matrix; reasons include the binary-options context and many complaints/refund demands).

20.07.2018: FIU analysis notes Sparkasse plans extraordinary termination and asks for instruction regarding remaining balances and future credits/receipts.

23.07.2018: Prosecutor seizes the bank balance.

- end of December 2018: Sparkasse Koblenz finally transferred the money to the Cologne prosecutor’s bank account.

The enforcement gap is measurable: Sparkasse’s SAR and termination planning come months after BaFin’s January ZAG action and after peer banks had already exited.

7) Issues identified by EFRI

The Südwestbank case demonstrates that BaFin possessed a rapid and bank-directed instrument. Its selective application raises the question of why the same approach was not extended to the main inflow account at Sparkasse Koblenz during the period of highest consumer harm (02 – 07/2018).

BaFin’s documentation from November 2017 to January 2018 shows that BaFin had a full understanding of the laundering activities of Treuer and Shvartsman (B2G GmbH). Still, no BaFin-originating referral to the prosecutor or the FIU is visible in the excerpts prior to early February 2018. The earliest documented trigger for StA Köln is the FIU dissemination dated 05.02.2018; BaFin’s written notification to StA Köln appears on 07.05.2018.

8) Transparency: EFRI’s IFG request and BaFin’s refusal to provide the file

EFRI filed Informationfreiheitsgesetz (IFG) requests on 05.11.2025 with BaFin and Deutsche Bundesbank, seeking the full supervisory record (BaFin file EVG 3-QF 5000-20170243 and related materials) to verify what was going on from October 2017 until the 2017 and until end of July 2018.

But:

BaFin denied full disclosure / refused to provide the requested file, citing confidentiality concerns (ongoing criminal case and institutional autonomy).

Deutsche Bundesbank had provided no substantive response as of January 2026 (per EFRI summary).

This is why EFRI publishes evidence matrices. Without disclosure, the public cannot audit supervisory decision-making—mainly when consumer harm hinges on timing.

9) EFRI’s questions (document-driven)

To BaFin

Why was §7 ZAG used swiftly against Südwestbank on 22.02.2018, but no comparable Sparkasse-directed restriction was undertaken?

- How did BaFin assess ongoing consumer risk between February and June 2018 once criminal proceedings were open and multiple banks had exited?

Did BaFin file its own SAR or formal AML escalation to FIU before 05.02.2018? If not, why not, given the early bank information requests and transaction visibility?

- Does BaFin also have consumer protection duties to observe?

- Has BaFin undertaken supervisory action against Sparkasse Koblenz due to its failure to stop processing payments in due time?

To StA Köln

Why is no Sparkasse-targeting seizure visible in the excerpt set until July 2018, despite FIU’s February dissemination and the criminal case opening?

To Sparkasse Koblenz

Why was the first documented SAR filed only on 12.06.2018, despite you having received information from BaFin about B2G GmbH’s activities already in November 2017 and later-described waves of complaints and refund demands?

Pls note: EFRI represents 15 European consumers who transferred their lifetime savings to scammers via the payment rails of B2G GmbH in the period March to the end of July 2018 (in total € 1.325.000)

For more detailed information, please see our matrix established based on the criminal file.